By Peter Tchir of Academy Securities

Betting that the “everything rally” will continue seems about as mature and responsible as two high schoolers hanging out in their parent’s basement and idolizing heavy metal bands, but that’s where I am right now.

Major Headwinds

There are two major headwinds that I see (there are probably many more out there, including a resurgence of inflation, but I either don’t see them as realistic or am dismissing them for now).

Geopolitical Risks

-

Support for supplying weapons to Ukraine is waning. The fighting is clearly at a stalemate. In all likelihood, the next phase of the war will feature a renewed Russian offensive later on this winter once the ground freezes. It will also be interesting to see if North Korean arms play a meaningful role.

-

Israel and Hamas. Israel is making progress towards eliminating Hamas as a military threat, but not without civilian casualties and difficulties maintaining support from its allies (more accurately, the citizens of allied countries). This effort is far more likely to be measured in months (not days), and the difficulties and risks of escalation remain. I continue to hear more concerns about supply chains, both due to the loss of production in Israel and also concerns for the safety of shipping in the region.

-

China and the U.S. The highly anticipated meeting between Xi and Biden (More Than a Photo Op) seemed to go well, although Biden’s use of the word “dictator” dampened the fireworks in the immediate aftermath. Nevertheless, the “easy” next step is to relieve tensions, either by reducing tariffs or by shifting the rules regarding various high-tech sanctions. The easy and short-term “fix” is both easiest for politicians and what I’m betting on (especially given all of the other high-level meetings that occurred between the two countries leading up to the Xi/Biden summit). I expect that we get news that is good for markets from here, and I would own some Chinese stocks here for a trade.

-

My view is that maybe geopolitical headwinds are more than priced in at the moment.

Recession Risks

-

Maybe we are already in a recession?

-

The unemployment rate shot up from 3.4% as recently as April to 3.9% in October. That 0.5% move in a 6-month period seems concerning. While the Sahm Rule is focused on 3-month moving averages, it is worth noticing.

-

I don’t need AI (though it would probably help) to tell me that something weird is going on with consumers and retailers. Even my inbox is flooded with “storewide” discount offers. We saw a similar trend in autos when mailings went from “we want your used car” to “have we got a deal for you with your trade-in” to “winter sales events.” That was a very useful indicator for the Manheim Used Vehicle Index, which continues to decline. Sure, with AI scanning emails, looking at social media advertising, and parsing through earnings calls, we’d probably have “better” information than my subjective view, but I’m running with the view that sales are slowing more abruptly than expected.

-

For the first time in years, I feel that if I wait, I will get a lower price. That’s just me, but I suspect that far more readers will agree with this statement than disagree with it. As unscientific as that is, I’m running with it – schwing!

-

-

It is difficult (and dangerous) to be wrong twice. As we wrote in the piece linked above, there is a danger in continually calling for a recession and being wrong! Actually, there are two dangers:

-

Someone (or me the strategist), who calls the recession, loses credibility.

-

People are surprised by the recession when it actually hits.

-

-

The only “logical” view is that if you called for a recession, you are very careful about making another recession call. “Everyone” got it wrong the first time, so you get a bit of a “free pass” on that mistake. Much like the Fed reporting “transitory” inflation, you don’t want to be wrong again, because getting a second “free pass” is difficult.

-

I suspect that there is a massive amount of good (even great) bearish analysis on the economy that is being held back, restrained, or otherwise not making the circuits because it would be too embarrassing to be wrong again!

-

It was easy to be bearish on Treasuries and point to supply and D.C. because “everyone” was talking about it, the media loved it, and it was working.

-

It’s been difficult to be bearish on the economy, because it hasn’t been working, the media hasn’t had the time for it, and being wrong would waste a good “free” pass.

-

-

So, I think that the economy is slowing rapidly and we may be in a recession by year-end (while all these various agencies finish their revisions sometime in the 2nd quarter of 2024). That risk is dangerous for risk assets! But the bulls have some time before those stories dominate the headlines for all the reasons above, and markets won’t get fearful until then.

Since I’m bearish on the consumer, jobs, and the economy, you can understand why I don’t feel the need to argue why inflation fears (at least for the next few months) aren’t high on my list of market worries.

The Tailwinds

There are many potential tailwinds:

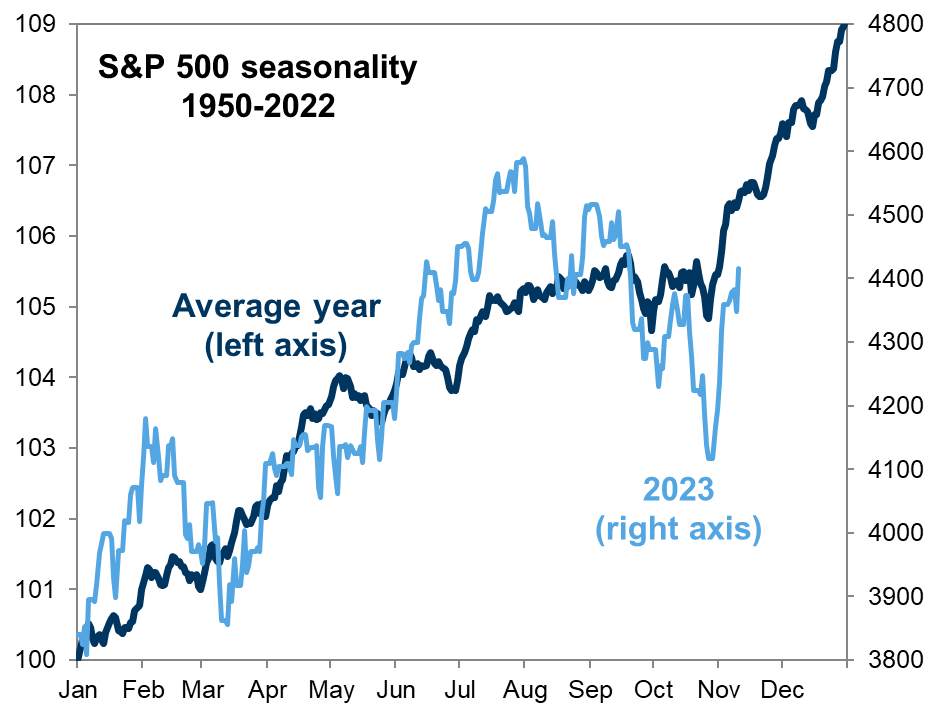

Seasonality. There is a reason why this report is sponsored by Wayne’s World. It is juvenile, simplistic, and entertaining (if not useful). We’ve made it to Thanksgiving, and sentiment has been and remains too bearish. There are plenty of reasons to talk about M&A (sellers have had enough time to lower their overly lofty expectations, and there is enough stability for buyers to step in, especially as financing costs got much more manageable in a very short time). All the year-end/Santa Claus rally stuff will get a lot of attention (more than usual) as the market’s recent strength will fuel the supply of such analysis. I don’t love seasonality, but who am I to fight it? Especially when it will help my market views

Rates.

The 10-year Treasury yield closed Friday at 4.43% (a level which it has bounced from recently). If yields go lower (I suspect that the data will help with this), then the next stop is around 4.3%. I see no reason for stocks not to respond well to yields as they head towards 4.3%. That is a number still “consistent” with a “reasonable” landing. Yes, we will start getting more and more recession calls in the coming days, but they will remain “background” noise and be easily dismissed. As we go below 4.3% that is when all those bears (who have been circumspect) will come out of the woodwork. So, lower yields (which is my main call) will help stocks until around 4.3% where the narrative will become more difficult (especially when the media and analysts will “unleash the hounds” of bearishness). It will take some negative news to reach 4.3% (given all the other issues). Lower inflation due to a better relationship with China can help initially, but we won’t be at 4.3% without some serious doubts about the state of the economy.

Return chasing. I am not worthy! Okay, I had to work that line into today’s report somehow, and this seemed to be the best place.

-

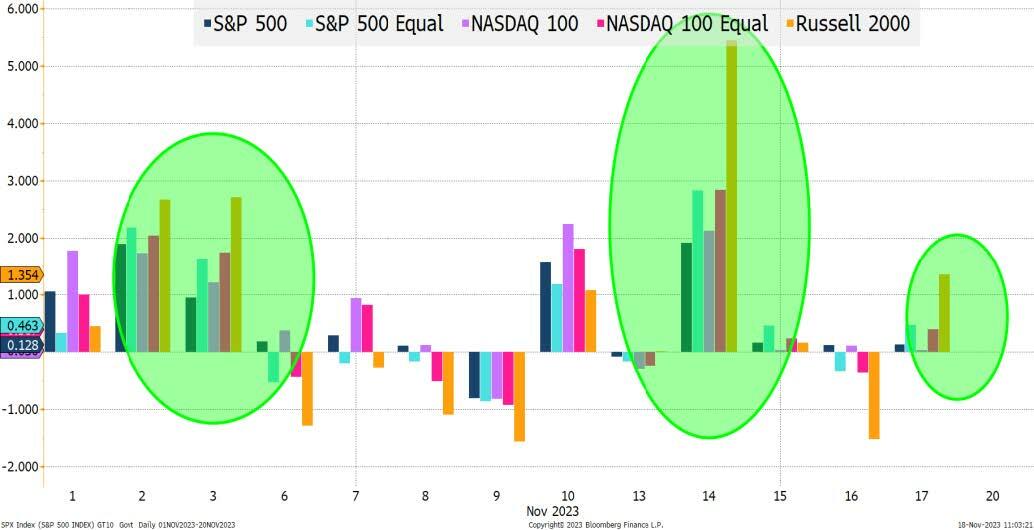

We all know how much of this year’s return has been driven by just a handful of stocks. The QQQ (a Nasdaq 100 ETF) is up 46% versus 22% for QQE (an equal weighted version). SPY (S&P 500) is up 19% vs 4% for RSP (an equal weighted version). IWM (Russell 2000) has eked out a 3.4% gain and was negative on the year as recently as last week!

-

Look at what is starting to happen as of late: the laggards have been driving the show, especially to the upside! On Friday, the “major” indices barely moved, but the equal weighted versions did well, with the Russell 2000 increasing more than 1% to gain over 5% on the week!

-

If there is one “pain” trade left for funds, it is being long the “magnificent” stocks versus being short everything else. If I was a massive hedge fund, one area that I’d try to squeeze higher into year-end would be the laggards (like the Russell 2000), partly because people are underweight or short, and partly because the market caps of companies in this index are smaller and they are easier to push around. I’m looking for a massive catch-up into year-end on the equal weights and Russell 2000!

The tailwinds might range from whimsical (seasonality) to technical (the laggards turning the corner) and rely on equities “misinterpreting” or “translating” lower yields “incorrectly” for a period of time.

Bottom Line

It may seem like some of my headwinds are tailwinds, but that is deliberate. Geopolitical risk is being priced in overly negatively at the moment, and I expect that news on the China/U.S. front will help mitigate risk.

It may seem like some of my tailwinds are headwinds, but that is on purpose. The move to lower yields will, at least initially, be more important than the reasons for those moves to lower yields.

I like rates and more inversion in the curves. Still using 4.3% on 10s as a near-term target.

I like credit. While we didn’t discuss credit directly in this report, I remain very bullish. Yes, supply will be higher than normal in December as issuers take advantage of the “unexpected” reprieve in rates, but there should be plenty of money available. That is especially true for BB issuers who can fill the void left in the BB space by Ford’s upgrade (Ford entities were upgraded by S&P to BBB- recently, making their bonds eligible for Investment Grade Index inclusion). I continue to believe that investors will rethink “credit” risk in terms of the U.S. government, and get more overweight credit products (please see last weekend’s Safety Dance where we try to explain this in greater detail).

Equities. I love the laggards and like the rest (for now). Use 4,600 on the S&P 500 as a target to watch (which seems like it could coincide with 4.3% on 10s), but be heavily skewed to the under-owned names, indices, and subindices as I think that the combination of positioning along with everything else will drive extreme outperformance!

Rally on! Schwing!

Just because something is juvenile and immature, doesn’t mean that it’s bad! Kind of like this “everything rally."