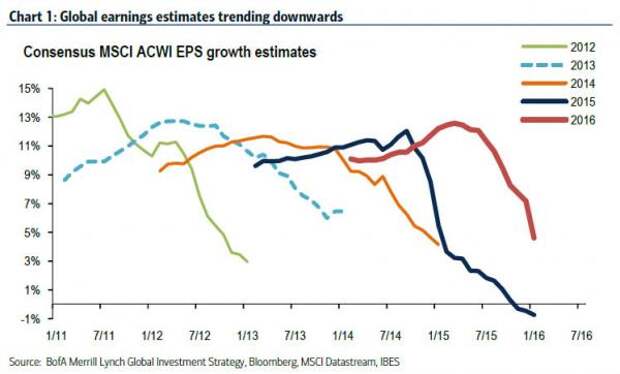

Several days ago, we showed the one chart which explains why Bank of America remains a stubborn non-BTFDer. This is what Michael Hartnett said last Thursday: "We remain sellers into strength in coming weeks/months of risk assets at least until a coordinated and aggressive global policy response (e.g.

Shanghai Accord) begins to reverse the deterioration in global profit expectations (currently heading sharply south – Chart 1) and credit conditions."

Since then things appear to have gotten even worse, because while not only is the almost concluded Q4 earnings season on pace to confirm yet another earnings recession, with a blended earnings decline of -3.8%, which according to Factset "will mark the first time the index has seen three consecutive quarters of year-over-year declines in earnings since Q1 2009 through Q3 2009", but both Q1 and Q2 2016 are looking just as bad: as Factset notes in its latest weekly update, "in terms of earnings, the estimated declines for Q1 2016 and Q2 2016 are -5.3% and -0.4%."

Putting this in perspective, just over a month ago, on December 31, 2015, the consensus for Q1 EPS was a growth of 0.8% vs a year ago. It is now down -5.3%...

... while revenues are likewise expected to drop by -0.1% compared to forecast incrase of 2.6% as of December 31.

As Factset then notes, as is usually the case, analysts are predicting significant increases in earnings and revenue growth in the 2nd half of the year. In terms of earnings, the estimated declines for Q1 2016 and Q2 2016 are -5.3% and -0.4%, while the estimated growth rates for Q3 2016 and Q4 2016 are 5.5% and 10.7%. In terms of revenues, the estimated declines for Q1 2016 and Q2 2016 are -0.1% and -0.1%, while the estimated growth rates for Q3 2016 and Q4 2016 are 2.3% and 4.5%.

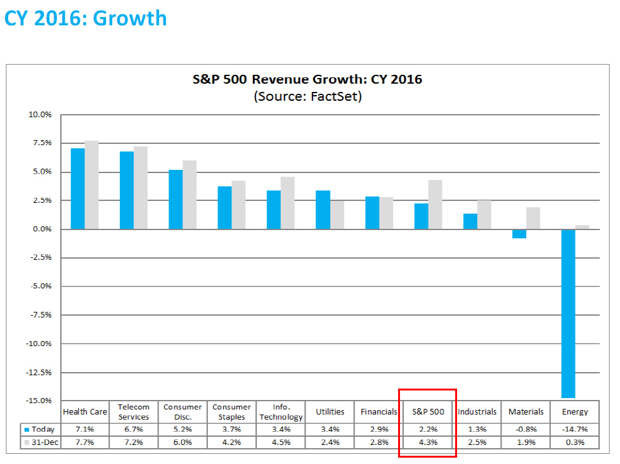

In other words, hockey sticks that would make any central bank proud. The only problem is that these forecasts will never materialize, which can be seen in the full year EPS forecast below. As highlighted in the box below, in just one month full year EPS has declined from 4.3% to 2.2%.

We open it up to readers to determine in how many weeks will full year 2016 EPS be revised tom 4.3% as of the start of the year, to 2.2% currently, to negative, indicating at least 7 consecutive quarters of declining EPS, something not recorded even during the peak of the financial crisis.

Incidentally, an earnings recession is two consecutive negative quarters of EPS: we don't know what the technical term is for seven...