Back in June, we explained that the reason behind the market's shocking response to the Fed's hawkish policy announcement when yields plunged instead of spiking higher, had little to do with what the Fed would actually do (as every Fed action is now in direct response to the market, which the FOMC is compelled to prop up no matter the cost) and everything to do with the market's read of r-star, and we quoted DB's head of FX strategy George Saravelos who said that everything that is going on "boils down to a very pessimistic market view on r*" or in other words, the same argument we made 6 years ago when we predicted - correctly - that the Fed's hiking cycle would end in tears (as it did first in November 2018 when the Fed capitulated on its hiking strategy after stocks plunged, and then again in Sept 2019 when the Repo crisis forced the Fed to resume QE).

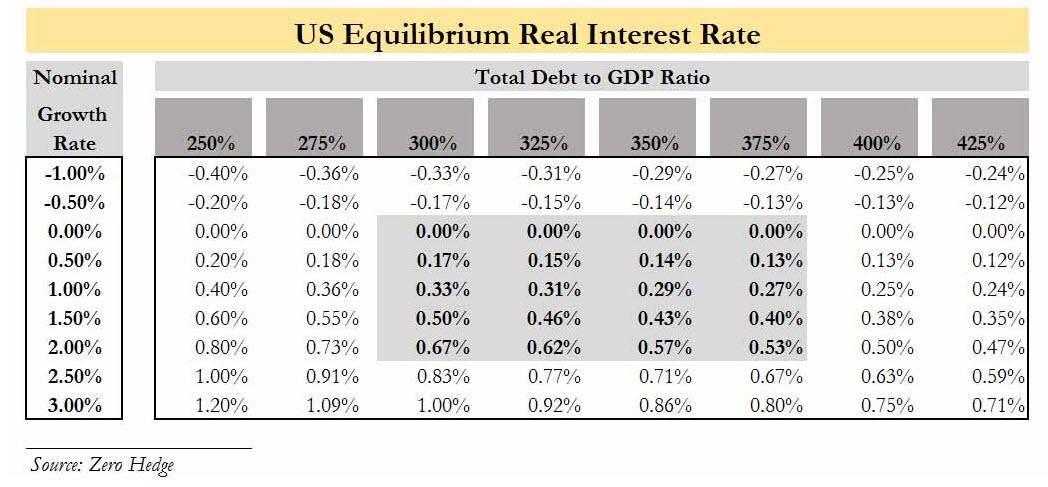

The bottom line, for those who missed our lengthy take on this complex topic is that the equilibrium growth rate in the US, or r* (or r-star), was far far lower than where most economists thought it was. In fact, as the sensitivity table below which we first constructed in 2015 showed, the equilibrium US growth rate was right around 0%. This means that each and every attempt by the Fed to tighten financial condition will end in disaster, the only question is how long it would take before this happens.

Today, we won't recap the profound implications from Powell's huge policy error which we laid out previously (we suggest readers familiarize themselves with our recent work on the topic published in "Powell Just Made A Huge Error: What The Market's Shocking Response Means For The Fed's Endgame"), but we will touch on a recent blog by Deutsche Bank's Saravelos - who unlike most of his peers on Wal Street, has a clear and correct read on what is currently going on in the market - and to help clients comprehend what's actually going on, he has penned a simple framework to understand current market behavior. As Saravelos puts it, "there is no “puzzle” in the way global bond markets are behaving and it is entirely possible for yields to fall as inflation pressures rise."

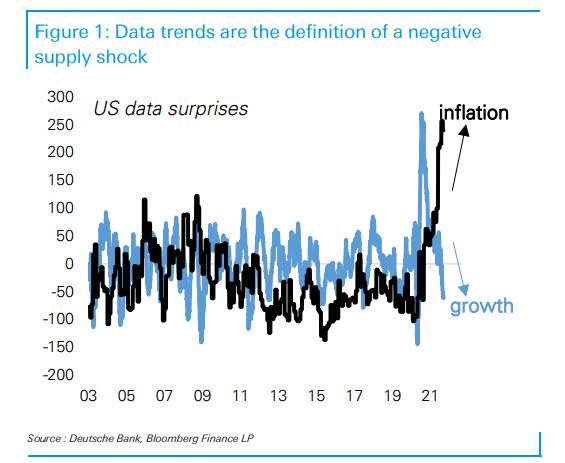

As Saravelos explains, the starting point is that over the last six months the global economy has been experiencing a negative supply shock due to COVID. This can be most clearly seen in the incredibly sharp run-up in inflation surprises against the equally incredible sharp run-down in growth surprises.

In simple Econ 101 terms, we are experiencing a leftward shift in the global economy’s supply curve. A negative supply shock (permanent or not) does two things: it lowers growth and increases inflation.

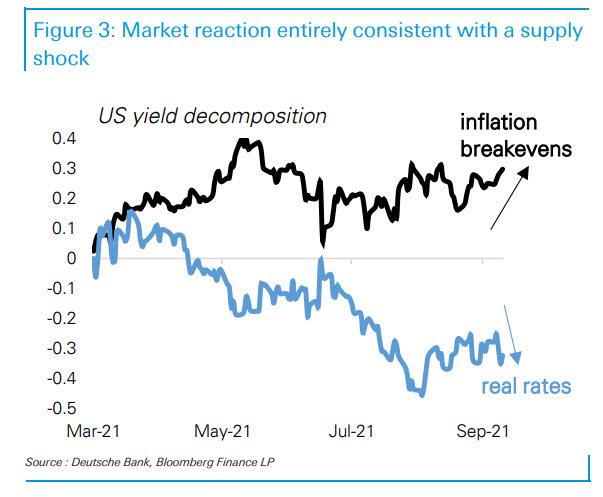

This is exactly what markets have been doing: inflation expectations are close to the year’s highs, but real rates (the closest market equivalent to a measure of real growth) are at the year’s lows.

The moves in the two variables are therefore entirely consistent with the incoming data.

Now what is most notable is that real yields have dropped more than inflation expectations have risen. The combined effect has been to lower nominal yields.

As Saravelos puts it, "there is nothing surprising about this, because there is nothing automatic about which effect dominates" and it ultimately depends on consumer sensitivity to rising prices, or in wonkish terms the slope of the demand curve: the greater the demand destruction from price rises, the bigger the negative effect on growth relative to inflation pushing yields down and vice versa. So, what the market is effectively doing, is pricing in substantial demand destruction from the supply shock.

Is this the correct thing to be pricing? Perhaps it is, we have been highlighting this unfolding demand destruction since May, and consumer confidence in the US is collapsing.

What about central bank reaction functions? There is an automatic belief in the market that higher inflation should mean more hawkish central banks. But as the DB strategist notes, "this belief rests on 30 years of demand shock management, where inflation has always and everywhere been positively correlated to growth." And as an interesting aside, according to Saravelos, Larry Summers was right about inflation risks this year but wrong about the cause: lower supply has dominated over stronger demand. A supply shock similar to the one we are currently experiencing means the central bank response is not obvious, and as a result "raising rates will only make the growth shock worse." By implication, tapering - which is tightening no matter what you read to the contrary - will similarly be a policy mistake and compound the economic slowdown, leading to an even more powerful easing reaction in the coming quarters.

Which brings us to central banks' characterization of the current inflation shock as transitory; as DB explains, it is another way of saying that they currently prefer to accommodate rather than respond to the supply shock. In terms of capital markets, ss long as the Fed looks through the shock, risk appetite will likely stay resilient, the dollar weak and volatility low. However, the moment the Fed does respond, all bets are off.

Bottom line, current market pricing is fully in line with a supply side shock with very strong demand destruction effects. A low r*, as we have been arguing since 2015 and again since June, is likely to prevail post-COVID only flattens consumer demand curves further. Saravelos concludes that "he continues to believe that it is the behavior of the consumer, including the desired level of precautionary savings as well as the response to the unfolding supply shock that is the most important macro variable for the market this year and beyond." As such, the latest UMich survey which showed that Americans are panicking over soaring inflation, and whose buying intentions have plunged to the lowest levels on record...

... is extremely alarming.